7 different approaches to budgeting

Because budgeting is a process of preparing detailed projects of future amounts, we can create a budget in many ways, including:

- top-down or bottom-up

- incremental

- zero-based

- rolling

- activity-based.

1. Top-down or bottom-up budgeting

Depending on the people involved, systems available, and the flexibility to plan and propose the budget, organisations can use a top-down or bottom-up budgeting approach.

A top-down budget is known as an imposed budget. It’s set without any participation by the ultimate budget holder.

A bottom-up budget is known as a participative budget. All budget holders can contribute.

2. Top-down budgeting

Points to consider about imposed/top-bottom budgeting style:

- It’s time-efficient because decisions are made by a limited number of senior managers.

- Junior managers might not have the skills to fully participate in the budgeting decision-making process.

- Senior managers have a better view of strategic objectives and the resources available.

- Senior managers are closer to the strategic objectives and have a long-term view of the organisation.

- Junior managers could build slack into the budget to make it easier to achieve.

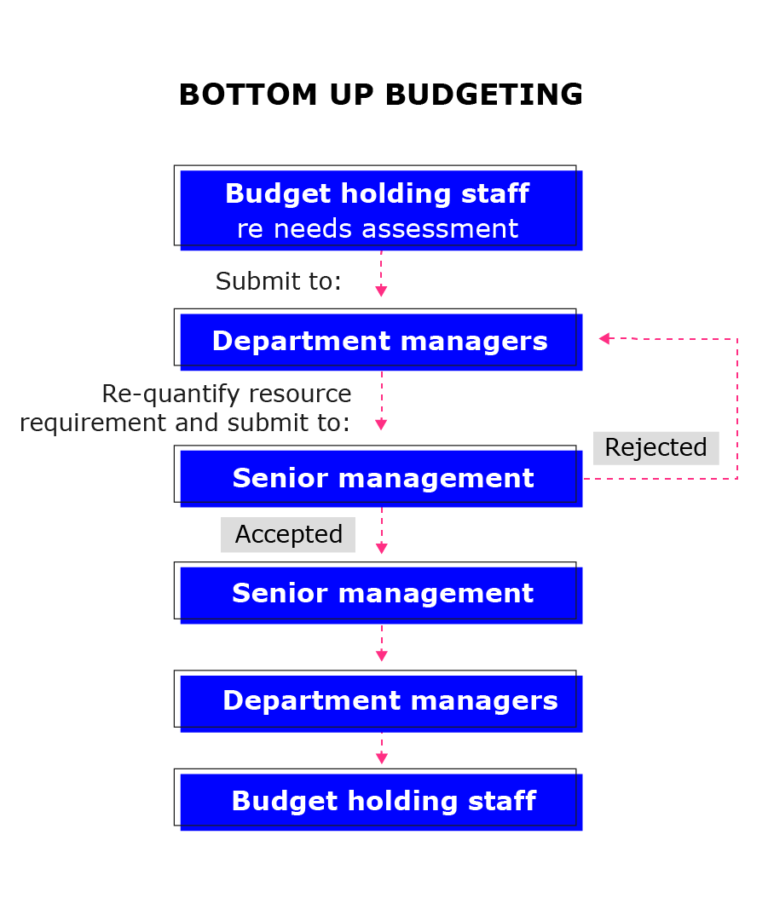

3. Bottom-up budgeting

Points to consider about participative/bottom-up budgeting style:

- Management’s morale is improved.

- Managers are more likely to achieve the plans in the budget.

- Lower-level managers are closer to the business and have better knowledge of unique issues/challenges and opportunities.

4. Incremental budgeting

Businesses often build on past budgets. The incremental budgeting process starts with the previous budget and adds (or subtracts) an incremental amount to cover inflation and other known changes.

Advantages:

- It’s quick and easy to maintain.

- It suits stable organisations with acceptable historic figures.

Disadvantages:

- It embeds earlier issues and inefficiencies.

- Economically inefficient activities can continue.

- It encourages artificial behaviour (i.e. spending the whole budget so the same amount is included in the following year).

5. Zero-based budgeting

Zero-based budgeting requires all costs to be justified by the expected benefits. It’s an alternative to incremental budgeting – the budget is based on the previous period’s budget or actual results, plus extra for inflation and other known changes.

Advantages:

- Inefficient and obsolete operations can be discontinued.

- There’s an increase in staff involvement because it requires a lot more information and engagement.

- It responds to changes in the business environment.

- There is efficient and effective resource allocation.

Disadvantages:

- It focuses on short-term benefits to the detriment of long-term advantages.

- The rigid budget process leads to lost opportunities.

- Management skills might be lacking.

- Staff might be demotivated by the need for significant time and effort.

6. Rolling budgeting

A rolling budget is continuously updated by adding an accounting period when the earliest accounting period expires.

Advantages:

- Planning and control are based on an accurate budget.

- It reduces uncertainty.

- The budget extends into the future.

- It encourages managers to reassess the budget regularly and more frequently.

Disadvantages:

- It’s costly and time-consuming.

- Staff might be demotivated by the time spent on budgeting.

- It can lead to less controlled results due to the effort required.

- Version control can be an issue because numbers are always changing.

7. Activity-based budgeting (ABB)

This budget is based on activities. Cost-driver data is used to set budgets and variance analysis.

Advantages:

- This system draws attention to overhead costs, which make up a large proportion of total operating costs.

- It recognises the activities that drive costs.

- It provides useful information for Total Quality Management (TQM).

Disadvantages:

- It takes time to identify activities.

- It’s difficult to identify responsibility for individual activities.

Types of budgets

Master budget

The master budget is a compilation of all the budgets. It’s similar to published financial accounts. It consolidates all subsidiary budgets and usually comprises the budgeted profit and loss account, balance sheet, and cash-flow statement.

Cash budget

A cash budget is a detailed estimate of the organisation’s cash inflows and outflows.

Capital budget

A capital budget facilitates decision-making on specific investment project choices. It provides guidance on the total amount of capital expenditure to commit.

Operating budget

An operating budget captures the revenues and income, and the expenses expected in the forthcoming period.

Budgeting has now evolved beyond traditional budgeting to include techniques such as better budgeting, advanced budgeting, and beyond budgeting.

Components of the master budget

The chart below shows how budgets interact in the master budget.

Financial Analysis for Business Performance: Planning, Budgeting, and Forecasting

Financial Analysis for Business Performance: Planning, Budgeting, and Forecasting

Reach your personal and professional goals

Unlock access to hundreds of expert online courses and degrees from top universities and educators to gain accredited qualifications and professional CV-building certificates.

Join over 18 million learners to launch, switch or build upon your career, all at your own pace, across a wide range of topic areas.