Perfect competition markets

Let’s start with perfect competition, which is at one extreme of the market structure spectrum described in the previous step.

The key characteristics of perfect competition are that there are a large number of firms, and the products are homogeneous and identical. The consumer has no reason to express a preference for any particular firm because of this. There is freedom of entry and exit into and out of the industry or market. Firms are price takers and have no control over the price they charge for their products. Each producer supplies a very small proportion of the total industry output. Finally, consumers and producers have perfect knowledge about the market. If one firm changes an aspect of the product, everyone knows.

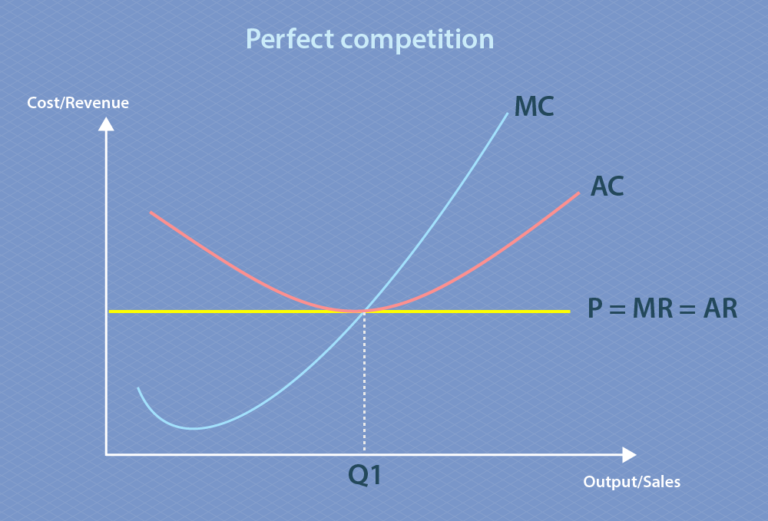

Now, let’s look at perfect competition graphically. The industry price is determined by the demand and supply of the industry as a whole. The firm is a very small supplier within the market and has no control over price. They will sell each extra unit for the same price. Therefore price = MR = AR, which is represented by perfectly elastic demand (ie a horizontal curve).

Select image to expand

Key to abbreviations:

AC – Average cost

AR – Average revenue

MC – Marginal cost

MR – Marginal revenue

P – Price

Q1 – Quantity produced

The MC is the cost of producing additional (marginal) units of output. It falls at first due to the law of diminishing returns, then rises as output rises. The average cost curve is the standard U-shaped curve. MC cuts the AC curve at its lowest point because of the mathematical relationship between marginal and average values. Given the assumption of profit maximisation, the firm produces at an output where MC = MR (marked as Q1 on the graph). This output level is a fraction of the total industry supply, because every firm in the market is also doing this. At this output, the firm is making normal profit. This is a long-run equilibrium position.

Short-run changes

We’re now going to look at what happens when something changes within a market with perfect competition.

In the graph below, MC1, AC1 and P1 represent the ‘start point’. Now assume a firm makes some form of modification to its product or gains some form of cost advantage, eg a new production method. What would happen? Average and marginal costs will be lower, but price, in the short-run, stays the same.

The lower average cost and marginal cost (represented by MC2 and AC2) would imply that the firm is now earning abnormal profit (AR1>AC2) represented by the grey area. The firm increases output (represented by Q2) in order to maximise on the profit it can make.

Long-run changes

Remember, the model assumes perfect knowledge, so all firms are able to make these improvements to their production processes. Therefore in the long-run, new firms enter the industry, attracted by the chance to make profit, and supply increases. This causes price to fall to P2, the firm is left making normal profit once again, and quantity falls back to Q1. Abnormal profit only exists in the short-run in markets with perfect competition.

Reach your personal and professional goals

Unlock access to hundreds of expert online courses and degrees from top universities and educators to gain accredited qualifications and professional CV-building certificates.

Join over 18 million learners to launch, switch or build upon your career, all at your own pace, across a wide range of topic areas.