Generic Reports and Communication Approaches

Generic reports and communication aren’t always appealing to an intended audience (who are never generic). Reports that are prepared without taking into consideration the recipient’s needs may not address the right business issues, and so are unlikely to provide relevant information to the user’s decision-making. Therefore, understanding your audience and their needs – and tailoring your communications accordingly – is critical to performance reporting.

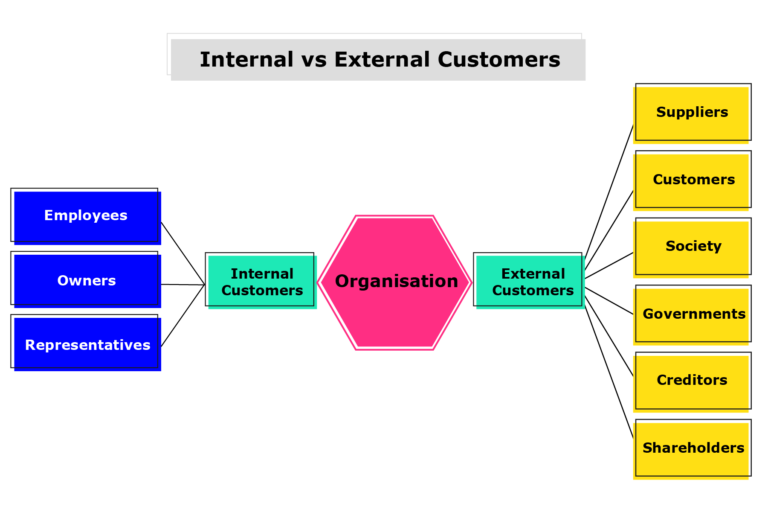

Types of audiences

There are different types of audiences who use financial reports and insights generated from such financial reports. Let’s take a look at some of the various stakeholders relating to a business or organisation.

Owners

Owners use financial reports to assess profit potential and the security of their investment. Historical financial performance can be used to forecast future financial performance. Security of investment will be based on the financial strength and solvency of the company. (Solvency refers to the ability of the company to meet long-term debt and obligations.)

Employees

Employees would be interested to know if the organisation can provide secure employment, as well as pay rises. In the current business environment, employees will also be interested in how the organisation is investing in developing their skills, capabilities, and overall well-being.

Representatives

Organisational representatives would include trade unions, committee representatives, among others. Such stakeholders will be interested in the well-being of the organisation and its financial position.

Suppliers

Suppliers would want to know if they would get paid on time. New suppliers would want assurances regarding the business’s financial stability before signing agreements.

Customers

Customers would want to know if the company can continue to supply goods and services, and informs them on the sustainability of its financial activities. Information regarding the financial position of the organisation and its profitability provides customers with a sense of the business’s continuity and reliability.

Society

Communities would want to know if an organisation will be able to continue its corporate social responsibility activities. By studying its financial statements, the general public can assess the impact of the company on the environment and the economy. For example, if the company has a cash flow bottleneck, it may have insufficient cash flows to fund planned financial activities.

Government

Government agencies need to know how the economy is performing to map out financial and industrial policies. Specifically, tax authorities are interested in financial statements and other analyses because they need to determine the amount of tax payable by an organisation.

Creditors

Loan providers (eg banks and creditors) need to know if a company can meet its short-term and long-term obligations. This depends on the solvency of the company, which can be assessed via the financial position of the company. Moreover, long-term loans could be backed by fixed assets; creditors would be interested in the value of these assets over time.

Now that we’ve looked at different stakeholders and their different reasons for being interested in an organisation’s financial reports and insights, let’s understand how to determine the financial reporting needs of different users.

Financial reporting needs

Financial reports are used by different stakeholders for different reasons. We can classify the types of financial reports based on the types of objectives and intentions. These include the following:

- financial performance

- financial position

- financing and investing

- compliance.

Let’s take a closer look at each.

Financial performance

The financial performance, or profitability, of an organisation, can be assessed by looking at the income statement. Stakeholders who are interested in financial statements to evaluate an organisation’s performance will look at the following information:

- cost of providing products and/or services

- change in the organisation’s control over resources during the reporting period

- the capacity of the organisation to generate sufficient cash flows from the existing resource base

- effectiveness and purposes for which the company has invested its cash flows.

Financial position

Financial positions can be reviewed by looking at the balance sheet, which could reveal the following information.

- The organisation’s control over its financial resources (eg liquidity). Its future distribution of cash flows. If the organisation is heavily debt-funded, the majority of future cash flows would be used to settle debts and obligations.

- The financial structure of the organisation, such as the proportion of debt vs equity funding.

- The ability of the organisation to attract and secure funding in the future. For instance, if the organisation is heavily debt-funded, it may not be able to secure more debt funding in the future.

- The solvency of the business and the ability of the organisation to meet its long-term financial obligations.

- The allocation of scarce resources such as factory space and machinery.

Financing and investing

The ways an organisation has financed its operations and invested its resources during the reporting period is valuable information to various stakeholders. By reviewing a business’s financial performance, stakeholders can see if the resources have been used for the intended objectives—and if they are achieving those objectives. The sustainability of the organisation can also be assessed by noting how investments are paying off.

Compliance

Compliance and regulation are important objectives for most stakeholders who use financial statements. They would use financial reports, analysis, and insights to assess how the company:

- is impacted by conditions imposed by borrowing agreements, licensing agreements, and granting agreements

- recognises spending mandates and borrowing limitations

- adheres to equal employment opportunity legislation

- adheres to occupational health and safety legislation

- adheres to environmental protection legislation.

Can you identify all the stakeholders in your business example? To support your understanding of this article, consider the diagram below and then create one for your business.

So far, we have discussed the importance of performance monitoring and reporting, and of tailoring your communication approach to meet the reporting needs of different stakeholders. With this in mind, the following discussion encourages you to identify and discuss any reporting habits you may have witnessed in any organisation you have come across. Reflecting on your professional working experience;

What are the current reporting habits that your organisation undertakes? If you’re not sure, what do you expect they should be?

Financial Analysis for Business Performance: Reporting and Stakeholder Management

Financial Analysis for Business Performance: Reporting and Stakeholder Management

Reach your personal and professional goals

Unlock access to hundreds of expert online courses and degrees from top universities and educators to gain accredited qualifications and professional CV-building certificates.

Join over 18 million learners to launch, switch or build upon your career, all at your own pace, across a wide range of topic areas.