Introduction to cost management and decision-making

One of the key findings of Deloitte’s 2019 annual global cost management survey was that if companies want effective cost management, they need to have in place:

- proper cost approaches and calculated decisions

- strategic reasoning behind their decision-making. [1]

Read: Cost management practices and trends in Europe and Belgium [1]

The general consensus is that companies without a strategic imperative struggle to effectively manage costs.

Over the past few decades, competitive pressure from the exponential growth in information technology, manufacturing technology, and service sectors has transformed how businesses operate. These major changes in the global economy have prompted the development of relevant and sustainable cost management practices.

Cost management and decision-making play a major role in improving business performance. Careful cost analysis helps managers, analysts, and business owners to determine total costs and helps clients to determine their expected invoice.

Cost management sets the preface for business costs and governs the actions to track the budget, to avoid going over budget. Cost-management decision-making creates a drive for better value at lower cost, to ensure projects are completed on time and are aligned with set goals and budget.

Accounting systems

Cost management systems help you to better manage business processes and customer needs. Let’s look at some related accounting systems that play important roles within the cost management information system.

Cost accounting

Cost accounting:

- applies cost accounting principles, methods, and techniques to control costs and ascertain profitability

- is concerned with preparing statements (eg, budgets and costings), cost data collection, and applying costs to inventory, products, and services.

Objectives

The objectives of cost accounting include:

- analysing and classifying all expenses related to products and operations

- calculating production costs and identifying inefficiencies to identify the extent of various forms of waste.

Cost accounting provides data for periodical income statements and balance sheets, and actual figures to compare with estimates for different periods. Analysing this information helps business managers with effective decision-making.

Scope

The scope of cost accounting includes:

- ascertaining costs

- controlling costs

- examining individual cost elements

- matching costs with revenue

- reviewing monthly or quarterly statements

- supporting decision-making.

Collecting, analysing, and measuring costs can be done either by post costing or continuous costing. Post costing uses actual costs, whereas continuous costing analyses costs after an activity is completed.

The scope of cost accounting also includes examining individual cost elements using a standard for each cost item and identifying variances. It also involves reviewing monthly or quarterly statements that reflect the cost and income data for an identified sale for that period.

Cost accounting helps you to identify cost-effective solutions, informs decision-making, and facilitates cost benefit analysis.

Management accounting

Management accounting:

- applies the principles of accounting and financial management to create, protect, preserve and increase value for stakeholders

- uses financial data and communicates it as information to users

- aims to create and increase value by providing relevant information.

Management accountants need effective communication skills to influence decision-making.

Management accounting was once part of cost accounting, but over time it evolved in function and scope. The terms are still often used interchangeably.

There are some underlying differences between the two, however, that you might want to consider before applying them to your business strategy.

| Characteristics | Cost accounting | Management accounting |

|---|---|---|

| Definition | Apply principles of cost accounting techniques and methods for cost control | Apply principles of accounting and financial management for preserving value of stakeholders |

| Function | Control cost and ascertain profit | Create and increase value by providing relevant information |

| Scope | Prepare statements, collect cost data, and apply costs | Use financial data to communicate information to users |

Read the following article if you would like more information on the evolution of management accounting.

Read: The origin and evolution of management accounting: A review of the theoretical framework [3]

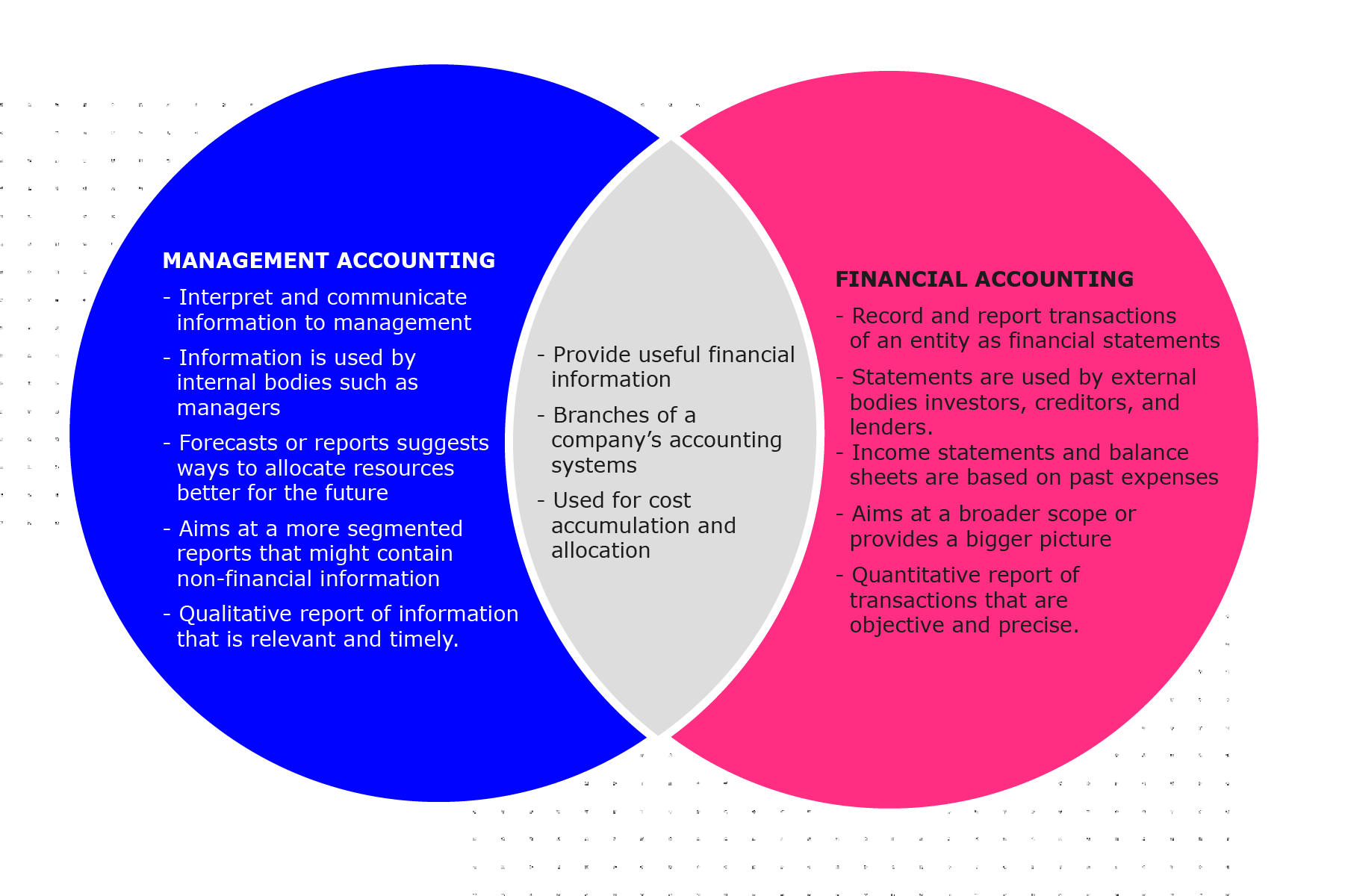

Financial accounting

Financial accounting is an accounting subsystem that:

- provides information to external users, such as investors and creditors—external users may use this information to buy bonds, sell and buy shares, or issue loans

- differs from cost management and management accounting primarily in its targeted users.

This video explains the similarities and differences between financial and management accounting.

This is an additional video, hosted on YouTube.

Here’s a summarised version of the similarities and differences discussed in the video.

References

- Save-to-transform as a catalyst for embracing digital disruption. Deloitte’s second biennial global cost survey: Cost management practices and trends in Europe and Belgium [Internet]. Deloitte. 2019 Sep. Available from: https://www2.deloitte.com/content/dam/Deloitte/be/Documents/strategy/2019%20European%20Cost%20Survey.pdf

- Waweru NM. The origin and evolution of management accounting: a review of the theoretical framework [Online journal]. Problems and Perspectives in Management, 8(3–1). 2010 Jul 14. Available from: https://www.researchgate.net/publication/287446113_The_origin_and_evolution_of_management_accounting_A_review_of_the_theoretical_framework

- Financial vs managerial accounting [Video]. Accounting Stuff; 2019 Mar 25. Available from: https://www.youtube.com/watch?v=qISkyoiGHcI

Financial Analysis for Business Performance: Reporting and Stakeholder Management

Financial Analysis for Business Performance: Reporting and Stakeholder Management

Reach your personal and professional goals

Unlock access to hundreds of expert online courses and degrees from top universities and educators to gain accredited qualifications and professional CV-building certificates.

Join over 18 million learners to launch, switch or build upon your career, all at your own pace, across a wide range of topic areas.