Budgeting for a district VISION 2020 programme

In this step we look how to budget for a district VISION 2020 programme and consider the most important resources to be managed: people’s time, and money.

This article is adapted from: Courtright P., Banzi J., Lewallen S. Budgeting for a district VISION 2020 programme. Comm Eye Health Vol. 18 No. 54 2005 pp 90 – 91.

Core concepts of a strong VISION 2020 programme

Many eye care professionals view the prospect of budgeting with about as much pleasure as a visit to the dentist! Nevertheless, for plans to succeed some basic skills in budgeting are essential.

Population based approach to planning and service delivery

A district plan is not a hospital programme but a population coverage programme. Targets for service delivery, e.g. number of cataract operations or spectacles needed, must be clearly defined before budgeting.

Efficiency reduces per unit cost

Achieving the goals of a plan will cost money; it will cost considerably more per unit of delivery if a surgical team is doing 300 cataract operations per year, than if a surgical team is doing 1,000 cataract operations per year because staff costs are a major contributor to overall cost per cataract done.

Adopting ‘bridging strategies’

A district plan may need to adopt a strategy for bridging the gap between communities and the hospital. There is insufficient evidence now to determine which strategies are most cost-effective, and it is likely that this will vary in different settings.

Budgeting

Prior to preparing a budget, targets for service delivery will have been set, and activities necessary to achieve these targets will have been agreed upon. These targets and activities, based on efficiency and priority, will drive budgeting. An example is shown in Table 1. It is helpful to consider three different types of costs in a programme.

Table 1. Targets and activities that determine the budget

| Targets | Activities |

|---|---|

| 1,600 cataract operations |

|

| 2,000 presbyopic corrections |

|

| 300 secondary school children to receive refractive correction |

|

| 20 children with congenital/developmental cataract to be identified and receive surgery (and follow up) at a tertiary centre |

|

Infrastructure-related costs

We have assumed, in our sample budget (Table 2), that there is already space dedicated for eye care at the district hospital as well as some equipment. If not, renovation or construction costs must be added. Building and equipment costs are one-time only expenses for building and for equipment. Lists of essential equipment are available in the IAPB Standard List of Medicines, Equipment, Instruments, Optical Supplies and Educational Resources for Primary and Secondary Level Eye Care Services. Do not forget non-clinical related equipment such as a vehicle and a computer.

Fixed costs

Salaries are fixed costs! Additionally, every month, regardless of the number of operations, water, electricity, and building rent or maintenance must be paid. These fixed costs should be included in the budget, no matter who pays them. Many districts will engage Ministry of Health personnel whose salaries are paid by the government and needs to be listed in a budget.

Variable costs

The cost of 1,000 intra ocular lenses (IOLs) is obviously more than 100 IOLs. Sutures, medicines, and other consumables are referred to as variable costs because the total cost for these varies depending on the number required. Bulk purchasing has to be based on expected output and limit wastage. In some settings consumables are donated; nevertheless, they should be listed in a budget, as they are real costs necessary for programme success.

Creating line items

There is no one ‘right way’ to create a programme budget. The details of preparing a budget come down to creating general categories with specific ‘line items’ in each category. For example, under the category of ‘transportation’ there could be line items such as petrol, vehicle maintenance and insurance, bicycle spares, bus fares, e.g. for team meetings or training or for bringing patients to the hospital for surgery. The category of ‘salaries’ will include each of the salaries of all the team members as individual line items.

‘Medical supplies’ can be another category, with IOLs, specific eye drops, and sutures listed as line items. Once all the real costs of carrying out a programme are listed, you may find that some of these costs are already covered; for example, government or other existing programmes may already cover some salaries. This is good as it demonstrates that you are using currently available resources and you can request less additional support.

Team input

Team input in developing a budget is essential. One person must be responsible for developing the budget, but he or she will need to consult with others on specific issues. The ‘manager’ must monitor on a regular basis how the actual expenditure compares to the budgeted costs and inform the whole team on how the programme is running.

Computer programs for budgeting

Although it isn’t essential, Microsoft Excel is an excellent computer program for creating a budget and monitoring expenses.

Conclusion

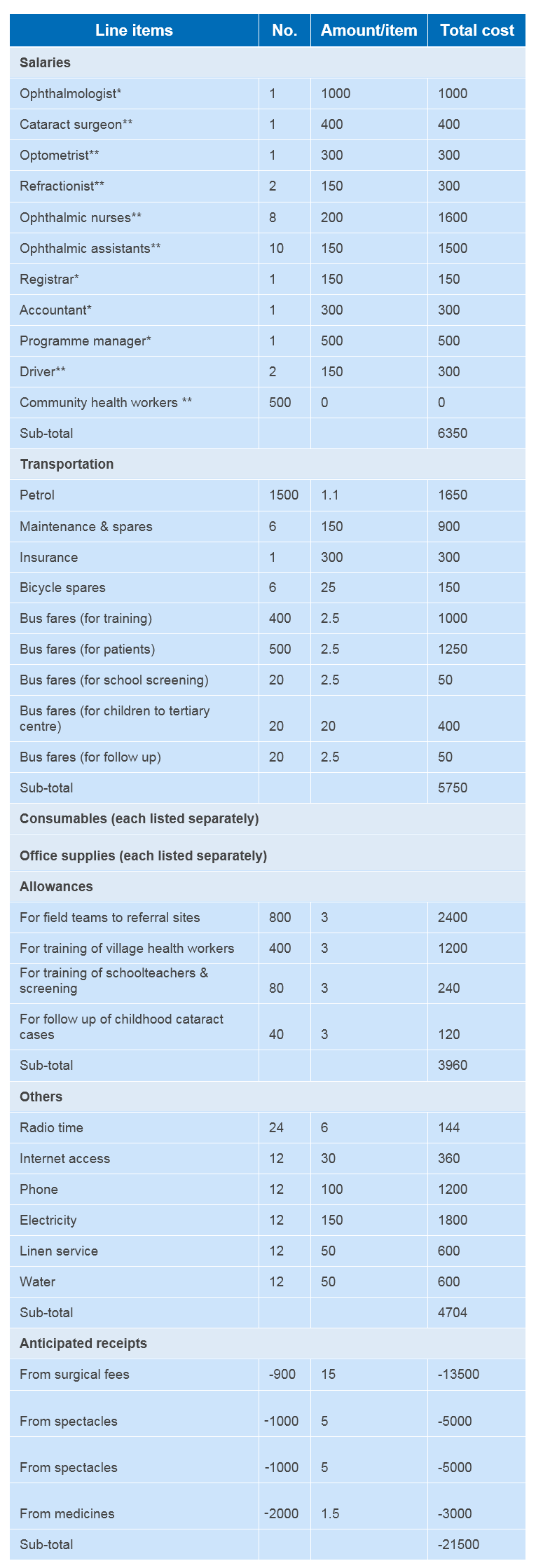

Finally, remember that a well-run district programme with a clearly thought out and practical budget will attract organisations interested in supporting these activities. An example of an outline budget for a district plan (targets shown in table 1) is given in table 2.

Table 2. Sample budget  Click to expand

Click to expand

Discussion

Which of the authors’ budgeting ideas and recommendations would you choose to apply, either in your own setting or in Zrenya our case study from week 2?

Global Blindness: Planning and Managing Eye Care Services

Global Blindness: Planning and Managing Eye Care Services

Reach your personal and professional goals

Unlock access to hundreds of expert online courses and degrees from top universities and educators to gain accredited qualifications and professional CV-building certificates.

Join over 18 million learners to launch, switch or build upon your career, all at your own pace, across a wide range of topic areas.