Accounting Analysis

When we analyse financial documents, it is easy to focus on the profit and value of assets as a guide to performance. However, accounts can yield more detailed information and have the potential to be analysed in multiple ways to provide a better picture of how they are performing. There are many performance categories that we can look at, but we will focus on two main ones within this course. These are profitability and liquidity.

Profitability is tied in to the earrings of a business and there are three useful calculations that can be applied. The first is the gross profit margin calculation. It is easy to look at increases and decreases in gross profits and make assumptions about performance. However, the gross profit margin scrutinises the value of the profit being made. This is done by measuring the profit as a proportion of the sales. In other words, it looks at how wide the gap is between the gross profit and the sales turnover. The formula for this is:

The answer will be displayed as a percentage figure and a company will compare the margins with previous years. The information from this calculator might be used to determine whether a company needs to find cheaper suppliers or whether it should increase the price of its products. Both of these actions can improve the gross profit margin.

The next profitability calculation is the net profit margin. This is very similar in function to the gross profit margin, but the focus is on identifying whether the company is paying too much in operating expenses. Therefore, to improve the figure, a company might look to see whether they can reduce their overheads and cut operating costs. The formula is displayed below.

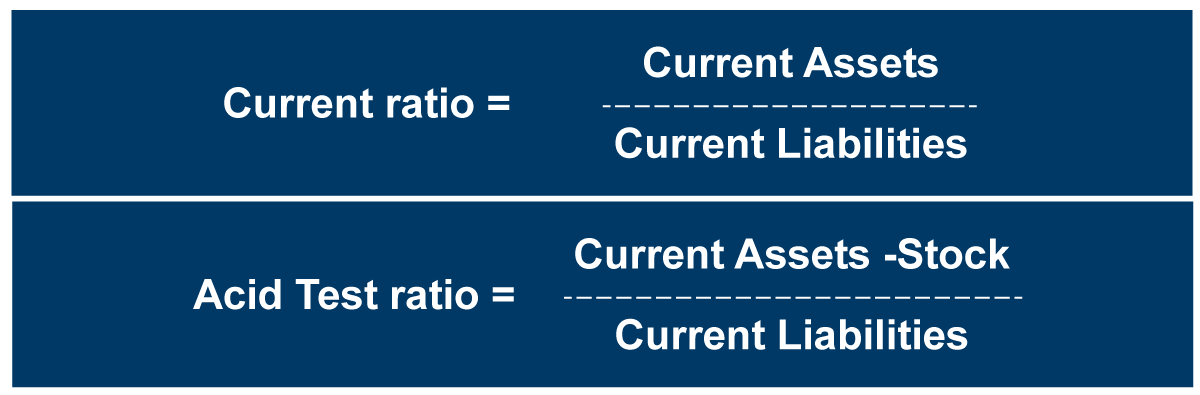

The liquidity ratios look at the ability of a company to pay off its short term debts with its current assets. There are two main liquidity ratios. These are the current ratio and the acid test ratio. The formulas for both of these are displayed below.

The ratio is expressed as a proportion to one. For example, a current ratio of 2:1 means that a company has twice as many current assets as it does current liabilities. This would be a good position to be in because a company can easily pay off the money it owes in the short-term using its current assets. If this figure were to be 1:1 it would not have enough current assets to pay off its debts and fixed assets might need to be sold. The acid test ratio removes stock from the current assets because stock is considered to be the most difficult current asset to convert into cash. This is because there is no guarantee that stock will be sold.

In interpreting the financial calculations it is important to do additional research that offers further insight. For example, certain industries have naturally high or low margins and the figure by itself does not reflect how a company has performed compared with others. Also, there may have been a number of external factors that were not in the company’s control, but had a positive and negative impact on the business. Therefore, it is important to ask further investigative questions. However, by comparing figures from previous years, a basic performance comparison is possible.

You will now have the opportunity to use some of this knowledge and analyse a set of accounts yourself.

Business Planning to Grow Successful Companies

Business Planning to Grow Successful Companies

Reach your personal and professional goals

Unlock access to hundreds of expert online courses and degrees from top universities and educators to gain accredited qualifications and professional CV-building certificates.

Join over 18 million learners to launch, switch or build upon your career, all at your own pace, across a wide range of topic areas.

{kind=link}

{kind=link}

{kind=link}