Food Cost Control Programme

The menu is not the only contributor to profitability, a chef or catering manager is responsible to ensure that there is a rigorous food cost control programme in place throughout food production, from designing the menu through to evaluating food cost results.

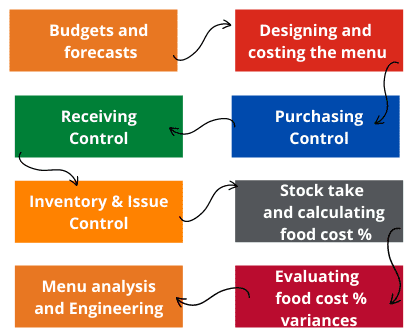

Elements of a cost control programme involve the following aspects:

We shall consider each of these briefly:

Budgets and forecasts

Budgets are defined as a financial plan and may be described as a realistic expression of management’s goals and objectives expressed in financial terms. Many businesses establish budgets for specific aspects of operation. Thus, there are sales budgets, cash flow budgets, capital equipment budgets, and advertising budgets among many other possibilities.

A forecast is a prediction of unit sales, or expressed in monetary terms, normally based on historical data.

For example:

| 400 covers | $6 500 per day | $35 000 per month |

Pre-costing menus

Your first control method is the pre-costing of your menu, to determine the exact costs of the menu items so that you can price your menu items and achieve the correct profit margin.

You need to prepare menus that achieve the maximum sales volume with the maximum profit, since this will increase your profit margin. In other words, you should try to sell many of the portions of food that have a low food cost. This will make your gross profit margin greater.

Purchasing control

Purchasing control involves ensuring that the best price for quality is obtained for food products. Generally, several quotations are received prior to purchase to ensure that the best price for the best quality of goods is received. Orders should be provided so that when the order is delivered, the quoted cost, quantity and quality can be compared against the delivery of goods.

Receiving control

When goods are received, they should be checked against the order for the correct cost, quantity, and quality.

Inventory and issue control

Inventory should be managed correctly, food should be stored correctly, including temperature controls, dated marked and the FIFO (First in First Out) system used to ensure that stock does not perish and get wasted.

When issuing food items these should be carefully counted out and only the required amount of goods issued that are required for production.

Security systems should be in place to protect against pilferage.

Stock take and calculating cost percentages

Because wastage can occur in the food production process and any of the other stages, regular stock takes should take place to ensure that physical stock amounts balance to the stock figures on stock sheets. Technology is making it easier to keep stock controls in place. If you would like to know more about technology in a professional kitchen, please look at our AI in a Professional Kitchen course.

Monthly food cost percentages should be calculated from stock takes and compared to the budgeted food cost percentage.

Evaluating food cost percent variances

Deviations from the budgeted food cost percentage should be evaluated. There are many reasons that the food cost percentage is higher than budgeted:

- Inaccurate counting of stock on hand

- Incorrect sales figures

- Loss through spoilage, pilferage, wastage

- Increased food prices

- Poor menu costing

- Lack of control during preparation for example not using standardised recipes and portion control

Are all reasons for food cost variance to budget.

Menu analysis and engineering

Menu analysis and engineering is one of the key control procedures used in maximising profits.

Although menu analysis can only be done using historical data (data that already exists). Menu analysis will help you to monitor and establish whether your efforts to maximise profits were effective. It also offers you some ways to improve the profitability of your menu.

When analysing menus to improve gross profit, you have various alternatives:

- You can reduce purchase costs.

- You can increase selling prices.

- You can change the entire menu to items that have a higher individual gross profit.

- You can substitute one or two items on the menu for more profitable or more popular items.

- You can stick to the more popular items on the menu.

Reach your personal and professional goals

Unlock access to hundreds of expert online courses and degrees from top universities and educators to gain accredited qualifications and professional CV-building certificates.

Join over 18 million learners to launch, switch or build upon your career, all at your own pace, across a wide range of topic areas.